NEW

✨ Health insurance, now in PayFit - learn more

LATEST

💷 All the rates & thresholds you need to know for 25/26...right here

WEBINAR

✨ The Payroll Journey: Start, Scale & Succeed Globally - learn more

✨ Health insurance, now in PayFit - learn more

💷 All the rates & thresholds you need to know for 25/26...right here

✨ The Payroll Journey: Start, Scale & Succeed Globally - learn more

Here are the essential points every UK employer must know about Statutory Maternity Pay:

A new baby is a significant life event for any employee. For HR, finance, and business leaders, it triggers a crucial set of legal and financial responsibilities. At the heart of this is Statutory Maternity Pay (SMP).

Understanding statutory maternity pay is not merely a compliance issue. It’s fundamental to supporting your people, effectively managing your payroll, and maintaining a healthy cash flow.

For growing businesses, navigating the complexities of maternity leave and pay can seem daunting. The rules on eligibility, payment rates, and reclaiming costs from HMRC are detailed, and also can change according to new legislation. Getting it wrong can lead to legal challenges, poor employee relations, and financial penalties.

This guide provides comprehensive information to help you manage SMP correctly, efficiently, and with confidence.

It’s vital to understand the difference between leave and pay. They are not the same thing, and employees can be entitled to one but not the other.

Statutory Maternity Leave (SML) is the time an employee is allowed to take off work. All female employees are entitled to 52 weeks of maternity leave, regardless of how long they have worked for you, or how much they earn. This is a day-one right enshrined in employment law. The 52 weeks are split into 26 weeks of ‘Ordinary Maternity Leave’ and 26 weeks of ‘Additional Maternity Leave’.

Statutory Maternity Pay (SMP) is the money an employer pays to an employee during their maternity leave. This is not a day-one right. It has strict qualifying conditions, and is only provided for 39 of the 52 weeks.

An employee who has been with you for four months, for example, is entitled to take the full 52 weeks off, but she will not be able to claim SMP.

To qualify, an employee must meet two key conditions, the continuous employment rule, and the earnings rule. And as the employer, it is your responsibility to verify these are met.

An employee must have been employed by you continuously for at least 26 weeks up to and including the ‘qualifying week’. This is the 15th week before the expected birth week.

This means you need to count back from that 15th week. The employee must have started employment with you on or before a date that gives them 26 weeks of prior service. And this period must include at least one day of work in the qualifying week.

In the ‘relevant period’ (usually the 8 weeks leading up to the qualifying week), the employee’s Average Weekly Earnings (AWE) must be at least equal to the Lower Earnings Limit (LEL). This is a crucial calculation, and understanding how to calculate weekly pay correctly is, in fact, foundational for all statutory payments.

LEL is the amount an employee must earn to qualify for certain state benefits and is the threshold where they start making National Insurance payments (even if they pay at a 0% rate).

If an employee’s average income is below this threshold, they will not qualify for SMP.

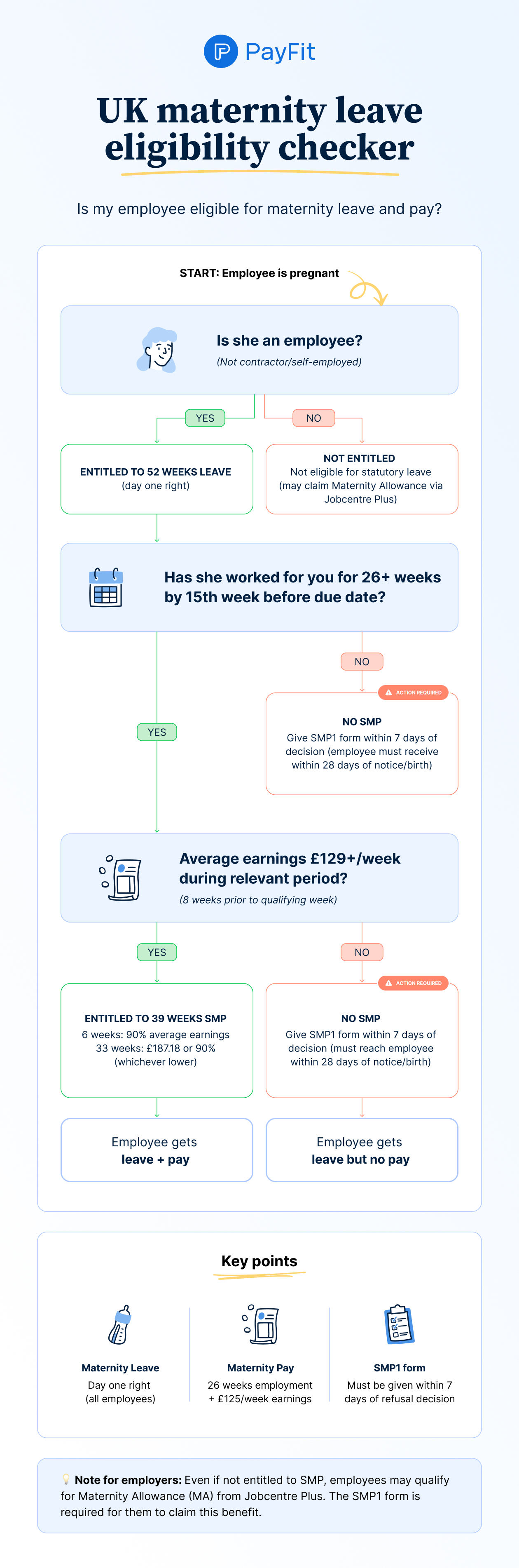

Determining SMP eligibility can be complex. Use our visual flowchart to quickly establish if your employee meets all the requirements:

If you find that your employee does not qualify, you cannot simply tell them so without giving them any explanation. Instead, you must provide them with an SMP1 form within 7 days of making the decision. This form will explain precisely why they are not eligible.

The employee can then use this form to ask the government for Maternity Allowance (MA). This is a separate allowance paid directly by Jobcentre Plus, not by you, and will ensure the new parent still gets financial help, even if they don’t meet the SMP criteria.

Once you’ve confirmed an employee qualifies, the next step is calculating their pay. SMP is provided for a maximum of 39 weeks. However, the amount they get changes during this period.

For the first 6 weeks off, the employee receives 90% of their AWE. There is no upper cap on this amount. You must calculate their AWE from the ‘relevant period’ you used for the eligibility test.

For the remaining 33 weeks, the employee is entitled to the standard government-set weekly rate, or 90% of their AWE, whichever is lower. The government reviews the rate each April:

2025/26 tax year: £187.18 per week

2026/27 tax year: £194.29 per week (confirmed increase of 3.8%).

If 90% of your employee's AWE is less than this (for example, if they work part-time), you would continue to pay them the 90% amount instead.

The Alabaster ruling means you must recalculate an employee's SMP if they get a pay rise at any time between the start of the ‘relevant period’ (used to calculate their SMP) and the end of their entire maternity leave. You must therefore recalculate their Average Weekly Earnings (AWE) using the new, higher pay rate, and then apply it retroactively as follows:

For the first 6 weeks: Their 90% pay must be based on the new, higher AWE, and you must pay them any arrears.

For the following 33 weeks: If their pay was 90% of AWE (because it was lower than the standard rate), this must also be recalculated and adjusted.

This applies to both individual and company-wide pay rises, and failing to recalculate can lead to legal challenges down the road.

A guide for businesses

Managing the administrative side of maternity pay is a key function for HR and finance teams.

To claim SMP, the employee must give you correct and timely information:

Notice: They must tell you they want to stop work to have a baby at least 15 weeks before the due date. They must also tell you when they want their leave and SMP to start. This date can be no earlier than the 11th week before the expected week of childbirth. If they change their mind about the start date, they usually need to give you 28 days’ notice.

Proof of pregnancy: They must give you a MAT B1 certificate. This is a form they get from their midwife or doctor, usually around 20 weeks into the pregnancy. It confirms their expected due date. You cannot make SMP payments without this.

If the baby is born early, or the expectant mother is off for a pregnancy-related illness in the 4 weeks before their due date, the leave starts immediately.

SMP is paid to the employee on their normal payday (e.g. weekly or monthly), and processed through your payroll system, just like their regular salary.

Crucially, SMP is treated as income. This means it is subject to all normal deductions, including PAYE tax and employee National Insurance. Employer NI contributions are also due on the SMP payment.

Running these payments correctly alongside normal salaries is a core function of your payroll. This is why many growing businesses find that using an automated payroll system is essential for accuracy and compliance.

This is the most critical part for finance managers. You are not expected to bear the full cost of SMP. You are, in effect, administering the payment on behalf of the government. This means that you can reclaim the money from HMRC.

Most employers can reclaim 92% of the SMP they pay. This recovery is done by reducing the PAYE and National Insurance bill you pay each month. Your payroll software should calculate this amount for you, which you will then report on your Employer Payment Summary (EPS) submission.

If your business qualifies as a ‘small employer’, you can reclaim 103% of the SMP. This means you actually get back more than you pay out, as a small credit to help with administrative costs.

You qualify for Small Employers’ Relief if your total Class 1 National Insurance contributions (both employer and employee) in the previous tax year were £45,000 or less. This is a significant benefit for many small and growing businesses.

If paying the SMP upfront would cause your business cash flow problems, you can apply to HMRC for ‘Advance Funding’, via the GOV.UK website.

SMP is just one aspect of an employee’s maternity. There are other important considerations to handle as an employer, such as KIT days, contractual schemes, and pensions. Some of these fall under UK employment law, which also governs Paternity Leave and Shared Parental Leave.

KIT days, or ‘Keeping in Touch’ days, are when your employee is allowed to work for you for up to 10 days during their maternity leave without losing their SMP for that week.

KIT days are optional and must be agreed upon by both you and the employee. As the ACAS guidance on maternity leave clarifies, neither party can insist on them. So, you must mutually agree on what working arrangements will apply and how much will be paid for them. This pay is considered separate from their SMP.

There are also SPLIT days, or Shared Parental Leave In Touch days. The difference between KIT and SPLIT is that the latter applies specifically to those on Shared Parental Leave.

As a business, you may choose to offer enhanced or contractual maternity pay. This is a company benefit where you pay more than the legal minimum (e.g. full pay for 3 months).

This is a powerful tool for attracting and retaining talent, and it’s worth considering as part of your wider employee benefits strategy.

However, the terms must be clearly stated in the employment contract, and the policy must be administered fairly. Managing different pay schemes is a task where a flexible benefits platform and an all-in-one HR software solution can be invaluable.

During the paid part of maternity leave (the 39 weeks of SMP), your employer pension contributions must continue. These contributions must be based on the employee’s normal, pre-leave salary, not on the lower SMP rate.

The employee’s contributions, however, are based on the actual SMP they are receiving. During the unpaid part of their leave, neither of you has to contribute.

For a growing business, manual SMP management can put you at significant risk of calculation and compliance errors. Calculating AWE, especially for employees with variable pay, is complex. And forgetting to issue an SMP1 form or miscalculating the 92% reclaim can cause legal and financial headaches. What’s more, the administrative burden on HR and finance teams is high.

On the other hand, modern payroll software automates this entire process, in order to:

Automatically calculate eligibility and the correct AWE.

Apply the correct 6-week and 33-week rates.

Accurately deduct tax and NI.

Generate the correct figures for your EPS submission, to ensure you reclaim the right amount.

Provide a clear audit trail for all payments.

This frees up your team to focus on strategic tasks, like coordinating and supporting the new parent’s return to work, rather than dealing with the mind-numbing number-crunching.

An employee has some choice, but there are some rules. The earliest they can choose to start their leave is on any day from the 11th week before the expected week of childbirth. They must give you the correct notice of their intended start date, which is usually by the 15th week before the baby is due.

However, there are two exceptions where the start date is automatic:

Early birth: If the baby is born early, their leave (and pay) starts automatically on the day after the birth.

Pregnancy-related sickness: If the employee is off work for a pregnancy-related illness in the 4 weeks before their due date, their maternity leave will start automatically the next day.

It’s also important to remember that all employees must take a minimum of 2 weeks of ‘compulsory maternity leave’ immediately after the baby is born (this is 4 weeks for factory workers).

They are still fully entitled to receive their Statutory Maternity Pay for the 39-week period, provided they met the qualifying rules. SMP is a legal right based on their past employment and earnings. You cannot ask them to pay it back. However, if you paid them enhanced (contractual) maternity pay, your company policy or the worker’s employment contract might state that the enhanced portion is repayable if they do not return for a set period.

It depends on their employment status. If a director is ‘employed’ (i.e. they have a contract of employment and are paid a salary through PAYE), they can qualify for SMP just like any other employee, provided they meet the earnings and service rules. Agency workers can also qualify if they meet the conditions, with the agency often being the responsible ‘employer’.

The government reviews these rates annually. The most accurate, up-to-date information is always published on the official GOV.UK website, on the employer guide to maternity pay and rates and thresholds pages. A dedicated payroll platform will also have these rates updated automatically, ensuring your calculations are always compliant, as you can see listed among PayFit’s many features.

For 2026/27:

SMP standard rate (weeks 7-39): £194.29 per week

Lower Earnings Limit: £6,708 annually (£559 monthly, £129 weekly)

First 6 weeks: 90% of AWE (no cap).

PayFit’s payroll software automatically calculates the SMP due, the relevant tax and NI deductions, and the exact amount you can reclaim from HMRC. This information is then used to generate your Employer Payment Summary (EPS), which is part of the HMRC RTI submissions process that PayFit fully automates, making the entire reporting and reclaim process seamless.

Our guide for UK employers & HR & Finance managers covers the essentials of statutory sickness pay & best practices for leave and absence management.

What is the Statutory Sick Pay (SSP) rate in the UK, and how do you calculate SSP for all of your staff? This guide explains it all.

Read about your responsibilities as an employer when it comes to paternity leave, from statutory pay to shared paternity leave, legislation and beyond.

Discover everything businesses need to know about UK maternity leave & pay in 2026, including statutory rates, eligibility, redundancy protection, KIT days.

Maternity leave is a statutory right in the UK for all female employees who are expecting or have had a child. Discover the specifics here.

A complete guide for UK employers on zero hours contract holiday pay, including 2026 updates, calculation methods, and statutory rights for irregular workers.

See what's new in PayFit

New features to save you time and give you back control. Watch now to see what's possible