NEW

✨ Health insurance, now in PayFit - learn more

LATEST

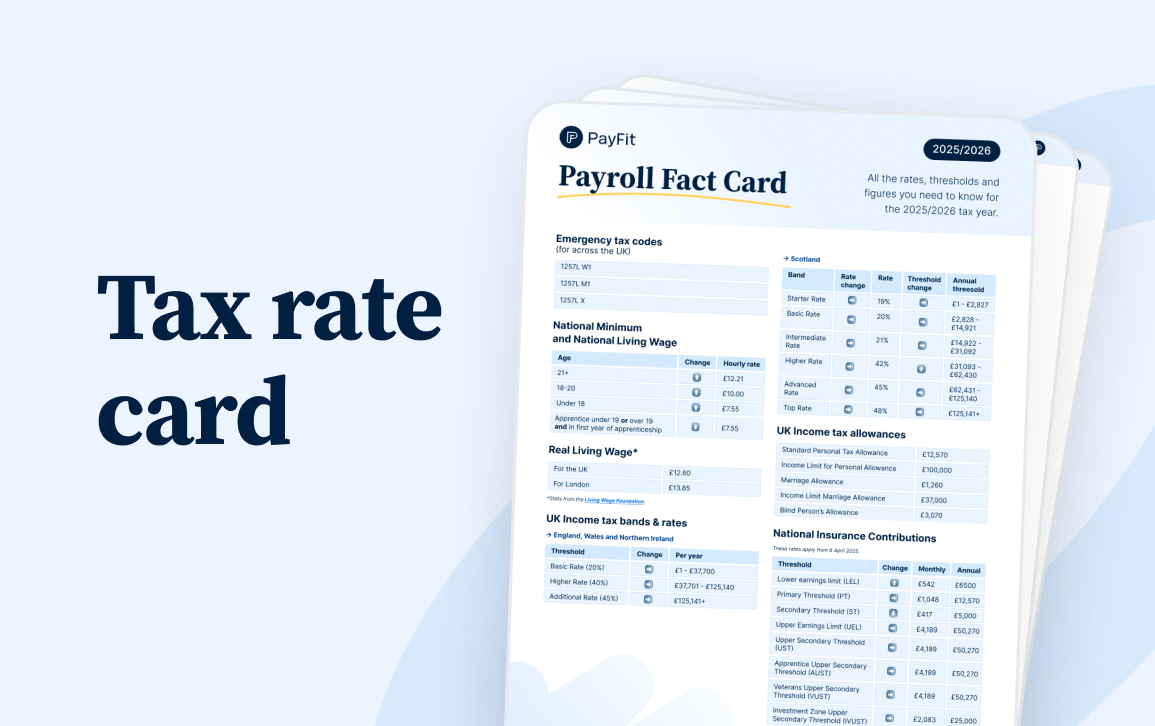

💷 All the rates & thresholds you need to know for 25/26... right here

WEBINAR

✨ The Payroll Journey: Start, Scale & Succeed Globally - learn more

✨ Health insurance, now in PayFit - learn more

💷 All the rates & thresholds you need to know for 25/26... right here

✨ The Payroll Journey: Start, Scale & Succeed Globally - learn more

UK employers are obligated by law to pay a percentage of employees’ earnings in National Insurance (NI) to HMRC via PAYE, as well as an additional contribution (referred to as employer National Insurance).

This guide will help you understand the different percentages of National Insurance that you’ll need to pay for each, and how these vary based on salary brackets and NI category letters.

So let’s dive into how to calculate National Insurance in the UK.

The amount of National Insurance employers are liable to pay depends on your employees’ employment status, and how much they earn. Most employees will pay Class 1 NI contributions (we wrote a handy article explaining all of the various NI classes here). This is made up of contributions deducted from employees’ gross pay and then paid to HMRC.

The amount paid also depends on the employee’s National Insurance category letter, and how much of the employee’s earnings falls within each category band.

Here’s a useful table to illustrate employee National Insurance rates, showing how much employers need to deduct from employees’ pay for the 2025/2026 tax year, depending on how much they earn per week or per month.

More information on category letters can be found in this Gov.uk article.

| Category letter | £125-£242 per week (£542-£1,048 a month) | £242.01-£967 per week (£1,048.01-£4,189 a month) | Over £967 per week (£4,189 a month) |

|---|---|---|---|

| A | O% | 8% | 2% |

| B | 0% | 1.85% | 2% |

| C | N/A | N/A | N/A |

| D | 0% | 2% | 2% |

| E | 0% | 1.85% | 2% |

| F | 0% | 8% | 2% |

| H | 0% | 8% | 2% |

| I | 0% | 1.85% | 2% |

| J | 0% | 2% | 2% |

| K | N/A | N/A | N/A |

| L | 0% | 2% | 2% |

| M | 0% | 8% | 2% |

| N | 0% | 8% | 2% |

| S | N/A | N/A | N/A |

| V | 0% | 8% | 2% |

| Z | 0% | 2% | 2% |

And here’s a table that illustrates how this applies when it comes to calculating National Insurance for employers.

| Category letter | £125-£242 per week (£542-£1,048 a month) | £242.01-£967 per week (£1,048.01-£4,189 a month) | Over £967 per week (£4,189 a month) |

|---|---|---|---|

| A | 15% | 15% | 15% |

| B | 15% | 15% | 15% |

| C | 15% | 15% | 15% |

| D | 0% | 15% | 15% |

| E | 0% | 15% | 15% |

| F | 0% | 15% | 15% |

| H | 0% | 0% | 15% |

| I | 0% | 15% | 15% |

| J | 15% | 15% | 2% |

| K | 0% | 15% | 15% |

| L | 0% | 15% | 15% |

| M | 0% | 0% | 15% |

| N | 0% | 15% | 15% |

| S | 0% | 15% | 15% |

| V | 0% | 0% | 15% |

| Z | 0% | 0% | 15% |

Looking at the first table above, if for example an employee is in category A and earns £4,500 a month (gross), you’ll need to deduct the following from their pay in employee National Insurance:

Nothing on the first £1,048

8% on their earnings between £1,048.01 and £4,189, which works out at £251.28

2% on the remaining earnings above £4,189, which is £6.22

This means that the amount of employee National Insurance contribution to be deducted from this individual’s gross pay and paid to HMRC is £257.50 for the month.

Again, using the same principle as above, and taking that same employee in category A who earns £4,500 a month, this is how to calculate employer NI, which you’ll need to pay in addition to employee NI.

15% on the first £1,048 - £157.20

15% on their earnings between £1,048.01 and £4,189, which works out at £471.15

15% on the remaining earnings above £4,189, which is £46.65

What this means is that, on top of the £257.50 you’ll need to deduct from the employee’s gross pay and pay to HMRC, you’ll also need to pay an additional £675 (from a separate pot of funding) in employer NI.

Employers are obligated to pay Class 1A and 1B NI on expenses and benefits provided to employees. The rate for the 2025/26 tax year is 15%. Class 1A payments are also due on some other lump sum payments, e.g.: redundancy payments.

You can learn more about NI classes in the blog we wrote on the topic, which can once again be found here.

Did those figures and tables make your head hurt a bit? You’re not the only one! Luckily, PayFit handles all of those calculations automatically, including NI due on expenses and benefits.

Once you plug in gross salaries, and specify the value of any benefits provided, all of the NI due is automatically calculated, added to your auto generated EPS / FPS, and then listed in a ‘payments to be made’ section. All you’ll need to do is pay HMRC (and, of course, your people, but you can automate that using PayFit as well!). How’s that for time savings?!

Rates & thresholds for 2025/26

Difference between gross and net pay in the UK (2026): learn how to calculate take-home pay, understand deductions and run accurate payroll.

Understand how to calculate UK payroll tax in 2026, including PAYE, Income Tax and NICs, with clear steps, current rates, and practical examples.

Pre-tax deductions UK explained for 2026/27: salary sacrifice, PAYE, statutory deductions and payslip rules to manage compliant payroll deductions

Ex gratia payment tax explained for 2026. Learn UK rules on the £30,000 exemption, how PILON and PENP are taxed, and how to stay HMRC compliant.

Payment after leaving HMRC guidance for 2026/27, covering final pay when leaving a job UK, tax code 0T, P45 and NIC rules for employers.

P45 form UK explained: learn what it contains, when employers must issue it, and how it prevents emergency tax codes for new hires in the 2026/27 tax year.