NEW

✨ Health insurance, now in PayFit - learn more

LATEST

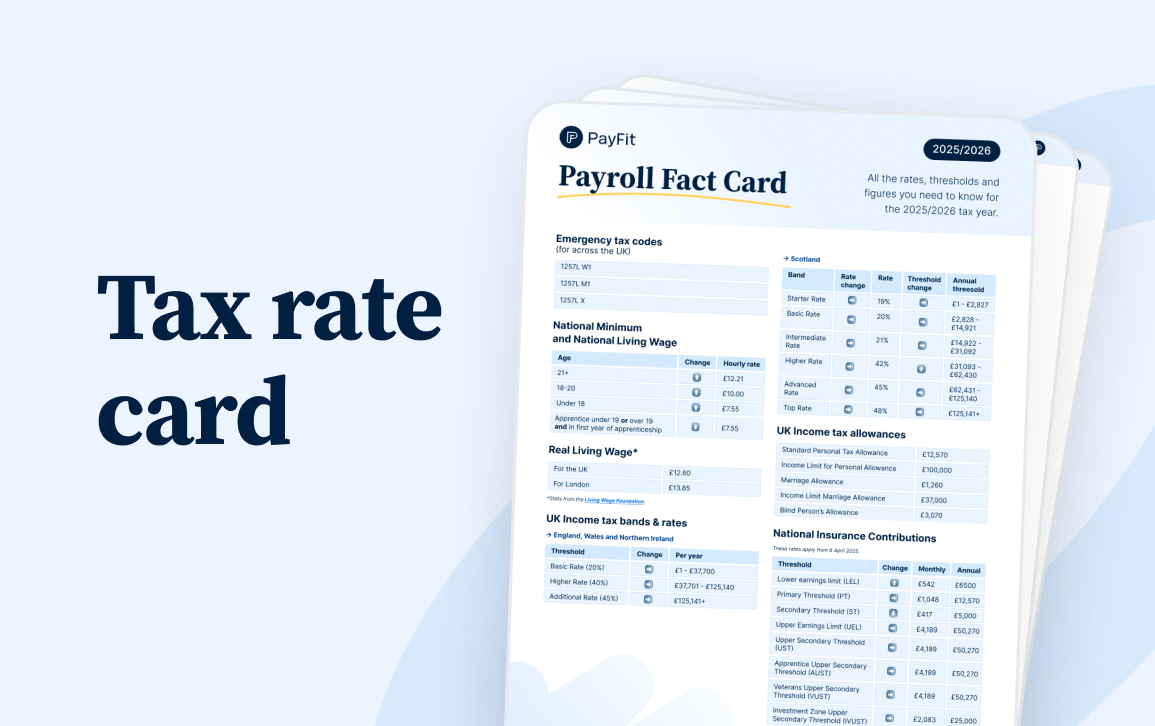

💷 All the rates & thresholds you need to know for 25/26... right here

WEBINAR

✨ The Payroll Journey: Start, Scale & Succeed Globally - learn more

✨ Health insurance, now in PayFit - learn more

💷 All the rates & thresholds you need to know for 25/26... right here

✨ The Payroll Journey: Start, Scale & Succeed Globally - learn more

If you’re an employer that pays Class I national Insurance for your staff, you can offset up to £10,500 per tax year from your Employer National Insurance bill.

This is what’s called the Employment Allowance, and is a great way for small businesses to pay less to HMRC and free up some funds for other initiatives. Very small businesses may even be able to pay no Employer National Insurance at all.

Find out more about the various Employment Allowance criteria and your eligibility as a small business below.

The allowance increased to £10,500 from 6th April 2025 (up from £5,000 in the previous tax year)

A government backed scheme that allows eligible businesses and charities to offset a portion (or all) of their Employer National Insurance Bill, the Employment Allowance is factored in each time you run payroll until the relevant amount of Class 1 National Insurance saving has been used up.

Businesses can claim up to £10,500 in savings each tax year, and you can still claim the allowance if your liability was less than this. If your Employer NI bill exceeds £10,500, you’ll just pay the difference. But if it’s under £10,500 per year, you’ll pay no Employer NI at all. However, you won’t be able to claim the difference (e.g.: you can’t claim back £8,000 if your bill is £2,500). The Employment Allowance can be claimed at any point during the tax year.

In order to be eligible, businesses must:

Have Class I NI liabilities of less than £100,000 in the previous tax year;

be registered as an employer;

have employees

The Employment NIC Allowance applies only to businesses (or charities), not individual employees. If your business is part of a group of companies, only one company can claim the allowance, and the total Class 1 NI liabilities must still be less than £100,000 across all the companies. The same applies if you have more than one payroll (i.e.: if you have more than one employer PAYE reference). Off-payroll workers should not be factored into your Class 1 NI liabilities.

How you claim the Employment Allowance depends on whether you’re already a user of payroll software or not. With a lot of software, it will simply be a case of selecting ‘Yes’ in the ‘Employment Allowance indicator’ field when you send an EPS to HMRC. Otherwise, you’ll need to download a free piece of software from HMRC called Basic PAYE tools.

With PayFit, however, it’s even simpler. Users simply edit their Employer registration details within the settings, selecting the ‘Claim employment allowance’ option. And that’s it - it’ll automatically reflect on your employer payment record report, which is submitted to HMRC on your behalf by PayFit, and the amount you owe is reduced. That’s one less thing to worry about!

See it in action for yourself by getting in touch and booking a demo of PayFit with a member of the team below.

Rates & thresholds for 2025/26

Learn how to register for Payrolling Benefits in Kind (PBiK) & simplify HMRC reporting. Discover 2025/26 updates & prepare for mandatory payrolling in 2027.

We explore the proposal for a £1,600 monthly universal basic income (UBI) trial in England, considering all the pros, cons and payroll implications.

The 2024 Autumn Budget has landed. What does the new Labour government have in store for businesses and their employees? We recap the top announcements made.

Read our guide to answer the question ‘what is small employers’ relief’, to find out how you can qualify as a business, and how much you can claim.

In this post, we’ll look at TUPE (Transfer of Undertakings Protection of Employment Rights), how it works and what employers need to know.

A recap of the 2024 King’s Speech, the announcements affecting businesses and their people teams and how HR leaders can adapt.

See what's new in PayFit

New features to save you time and give you back control. Watch now to see what's possible